Are you concerned about your Medicare out-of-pocket maximum? If so, continue reading to learn what to expect and how to even eliminate most out-of-pocket healthcare costs.

With the rising cost of healthcare, being covered by Medicare may not be enough. Many Medicare recipients are spending about 20 percent of their annual income on out-of-pocket costs not reimbursed by Medicare. Those who have lower incomes or complex medical conditions will likely pay the most and might not be able to afford it.

Easy Article Navigation

Determining your Medicare out-of-pocket maximum is a complex process. It changes depending on your health circumstances and your need to visit doctors and specialists. Fortunately, there are Medicare Supplement plans that can fill these gaps in coverage and mitigate your out-of-pocket expenses.

Here, we’ll take a look at the Medicare out-of-pocket maximum and determine the best method in reducing them year after year.

Where do Medicare Out-of-Pocket Expenses Come From?

Original Medicare is offered in four parts with each of them containing gaps in coverage that result in out-of-pocket expenses:

Medicare Part A – Even though Part A is free to most people, there is no out-of-pocket maximum which means the enrollee will find it difficult to budget for these eventual expenses. These expenses are the result of deductibles and limited coverages.

Medicare Part B – In Part B, you pay a monthly premium and an annual deductible before your coverage kicks in. There is also a limit to what healthcare costs Medicare will cover, but still no limit on the amount you’ll pay over the Medicare out of pocket maximum.

Medicare Part C – Medicare Part C (Medicare Advantage) is a government-subsidized health plan offered by private companies that combines your Medicare Part A, B, and prescription drug coverage. You’ll pay different premiums, deductibles, coinsurance, and other out-of-pocket expenses depending on the plan you choose. However, there are limits and once reached Part C (Medicare Advantage) will start paying 100% of covered expenses for the remainder of the year.

Medicare Part D – Similar to Part C, Medicare Part D is offered and administered by private insurance companies authorized by Medicare. Once Part D policyholder reaches the “catastrophic” phase in Part D, their prescription drug expenses will be limited to 25% of the cost of the prescription.

Current Out-of-Pocket Expenses while Covered Under Medicare

Although out-of-pocket expenses continue to go up as the cost of healthcare goes up, little has changed with Medicare’s coverage under Part A, Part B, and Part D.

In fact, the deductibles and monthly premiums for Medicare Part B continue to creep up as the cost of healthcare creeps up. There are no out-of-pocket limits under Medicare and that will likely continue as the government struggles to meet the cost of Medicare for seniors and individuals under 65 that medically qualify for Medicare.

Your Out-of-Pocket Costs for Part A

Medicare Part A is designed to cover hospital costs but most people receive this coverage with no monthly premium required.

The deductible for part a deductible increased in 2022 from $72 to $1,556. This deductible is not an annual deductible but rather a deductible per benefit period. This means if you are hospitalized with an illness or injury and recover you will be responsible for a $1,556 deductible.

However, if you are hospitalized later in the year for a different injury or illness the treatment you receive will also be subject to the deductible because the additional hospital stay is considered as a different benefit period.

Additional Part A out-of-pocket expenses result from Part A’s daily out-of-pocket costs when admitted to the hospital:

| Number of days in the Hospital | Daily Out-of-Pocket Expense |

| 1 to 60 days of inpatient care | $0.00 |

| Days 61-90 | $371 per day |

| Days 91+ of inpatient care until coverage is exhausted | $742 per day |

| After you’ve exhausted your 60 lifetime reserve days | All expenses |

As we mentioned previously, your deductible is applied to each benefit period. According to Medicare.gov, a benefit period is defined as follows:

A benefit period begins the day you’re admitted as an inpatient in a hospital or SNF. The benefit period ends when you haven’t gotten any inpatient hospital care (or skilled care in a SNF) for 60 days in a row. If you go into a hospital or a SNF after one benefit period has ended, a new benefit period begins. You must pay the inpatient hospital deductible for each benefit period. There’s no limit to the number of benefit periods.

Costs for a Staying in a Skilled Nursing Facility

If you require care in a skilled nursing facility, the benefits vary. For the first 20 days, you don’t need to pay a dime. But from day 21 to 100, your out-of-pocket costs will be $194.50 per day in 2022. From day 101 and thereafter you will be responsible for all costs.

Out-of-Pocket Costs for Medicare Part B

Medicare Part B pays for your outpatient healthcare. The monthly premiums are a portion of your out-of-pocket expenses and will vary based on your annual income. Part B also has an annual deductible ($233 in 2022) which must be met before Medicare will kick in.

As was stated earlier, there is no out-of-pocket maximum for Part B healthcare costs. An overview of the various out-of-pocket expenses associated with Part B are as

| Monthly Premium | Starts at $170.10 and adjusted upward with higher incomes |

| Per Year Deductible | $233 for all beneficiaries |

| Coinsurance | 20% on most healthcare costs but no coinsurance for preventive services |

| Out-of-pocket Maximums | None |

Medicare Part D Out-of-Pocket Expenses

Your Medicare Part D (if elected) is what covers self-administered prescription drug expenses. Since Part D is being offered by private insurance companies approved by Medicare, your monthly premium can vary by the company you select.

Typical Medicare Part D out-of-pocket costs are as follows:

The annual deductible – $480 for 2022

Your Monthly Premium – This amount will vary based on the company you choose and your level of income.

Coinsurance (copayment) – This amount will vary based on your prescription and is payable after you’ve met your annual deductible.

Coverage Gap – Also known as the “donut hole” you will enter the coverage gap once you and your insurer have spent $4,430 during the year. When you enter the coverage gap phase your coinsurance for prescriptions drugs will be 25% for both brand-name drugs and generics. Additionally, while in the coverage gap (donut hole) you could actually spend less on Tier 3 drugs but more on Tier 1 and 2.

Once your out-of-pocket expenses reach $7,050 you will exit the coverage gap and enter the catastrophic phase.

Catastrophic Phase – If or when you enter the catastrophic phase, your prescription drug coinsurance is reduced to 5% or a copayment, whichever is greater for the remainder of the year.

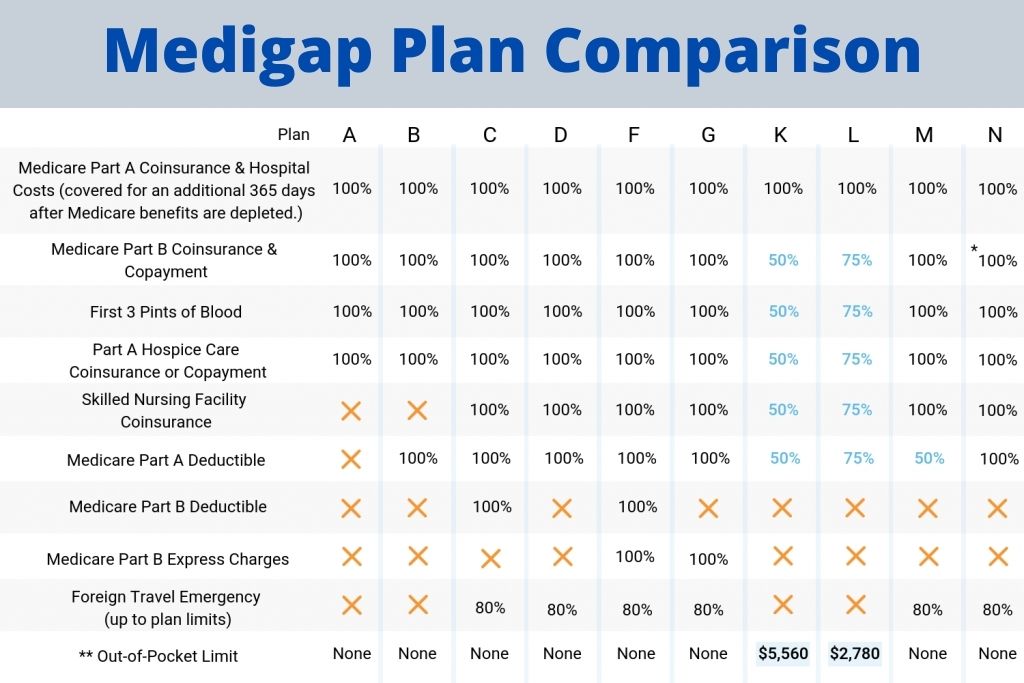

Medicare Supplement Insurance (Medigap)

Many seniors turn to a Medicare Supplement plan to minimize their out-of-pocket healthcare expenses. Medicare Supplement plans are offered by private insurance companies and are designed to fill in the gaps resulting from Original Medicare’s deductibles, copays, and coinsurance.

Currently, there are 10 Medigap plans to choose from and although the benefits are standardized among all insurance carriers that offer them, the difference you’ll find among the insurance companies is the price of the plans.

For example, a Medigap Plan G sold by Company A is the same as Medigap Plan G sold by company B. The differences between the plans will be the price of the plan and any additional benefits (not coverage) that each company offers.

Here, we’ll compare Medicare Supplement Plan N from four of the leading Medigap insurance companies for a 65-year-old male living in Georgia:

| Insurance Company | Plan | Monthly Premium |

| Assured Life | N | $98.90 |

| Aetna | N | $103.71 |

| Humana | N | $128.85 |

| BlueCross BlueShield | N | $131.00 |

The Medicare Supplement Plan N will take care of most out-of-pocket healthcare expenses required in traditional Medicare except for the Part B deductible and Part B excess expenses.

Considering a Medicare Plan?

Get online quotes for affordable Medigap insurance

To compare coverages offered by the 10 standardized Medicare Supplement Plans available in 47 states, please see the Medigap Comparison Chart below:

Have Questions?

We can Help!

Talk to one of our licensed Medicare supplement agents about the options available to you in your area.

Mon – Fri 8:00 am – 6:00 pm

Sat available upon request