What is Plan N Medicare Supplement

Medicare Supplement Plan N is coverage that’s meant to pay for many of out-of-pocket expenses which may otherwise not be covered by Part A and Part B of Medicare. It offers a list of comprehensive benefits which are like Medigap Plans G and F.

When you’re looking for a Medicare plan, you may have heard about this plan called Part N, Medigap Plan N, plan N Medicare, or even Medicare Plan N. True to its name, it is a supplement to Original Medicare. Parts refer to Original Medicare, and Plans refer to Medigap.

The advantage of Plan N is that people enjoy lower premiums, making it an attractive option For a personalized consultation on Medicare supplement plans and each insurance company that offers them call us at 844-528-8688. Although there may be many Medicare Supplement Plan N reviews to research, here we’ll drill down into Plan N to help you make an informed decision.

What’s Covered in this Article

- What Does Medicare Plan N Cover

- Medicare Plan N Cost

- How to Enroll In Medicare Part N

- Medicare Plan N vs. Plan G

- Medicare Plan N Vs. Plan F

- Frequently Asked Questions

Considering a Medicare Plan?

Get online quotes for affordable Medigap insurance

What Does the Medigap Plan N Cover?

Medigap Plan N coverage fills the coverage gap om four basic areas, which are of importance to just about anyone.

- Medical Expenses – The policy pays Part B coinsurance, except for a small copay for office visits and ER. It pays the rest of the 20% of Medicare-approved expenses, after a small Medicare Part B deductible.

- Hospitalization – It pays Part A deductible and coinsurance and will provide coverage for around 365 additional days after the Medicare benefits end.

- Hospice Care – It mainly pays Part A coinsurance

- Blood – The first three pints of blood are paid for each year. The original Medicare will then pay for any more pints needed that year.

- Foreign Travel Emergency

Medicare Supplement Plan N usually pays for nursing facilities and the Medicare Part A deductible for hospitalization. Here is the Medicare Plan N outline of coverage:

If your state allows charges above and beyond your Medicare copay, you are responsible for those costs. But if your doctor accepts assignment from Medicare (meaning they will accept a set fee for all services), excess charges are rare.

What Will Medicare Supplement Plan N Cost?

As with any other type of insurance policy, the Medicare Supplement Plan N rates tend to differ based on your location, the company, and insurance.

However, just for reference, in 2021, a 65-year-old woman who has no history of smoking and living in Florida will expect to pay between $120 and $180 monthly for Medicare Supplement Insurance Plan N. As you can see, there is a $60 difference variation for this exact same person because the insurer considers other variables.

So, the question is, how does an insurer set the rates for premiums for its Medicare Supplement insurance? Well, they use three price rating systems to help set premiums:

- Issue-age-rated – One of the factors that the premium is based on is your age at the time of purchasing the policy. That’s why it will cost less for younger people. However, the premiums can’t be raised after the issue date.

- Community rates – Generally, everyone with a Plan N will pay the same price, regardless of how old they may be. However, pricing still changes slightly based on inflation trends, but the insurer can’t raise the price because you’ve become older.

- Attained age-related – This means that the premium may start low and then become more expensive as you age.

There can be a wide range of price differences, mainly if the insurance company sells the policies at a discount versus regular prices or if the insurance company uses medical underwriting to determine if you’re eligible for Medicare. When in the market for Medicare Supplement insurance, we strongly advise that you compare apples to apples.

In other words, you should compare a Medigap Plan N from insurance company ‘A’ with a Medicare Plan N from insurance company ‘B.’ You never want to compare one company’s Plan N with the other company’s Plan B, because that way, the results you get are skewed, especially as far as the prices and benefits you can expect come in. Fortunately, our website allows you to easily compare plans by just entering your zip code.

View Plan N Quotes-

View Plan N Quotes-

How To Enroll in Medigap Plan N

People should enroll in the program as soon as they turn 65 and are eligible for coverage under Medicare Part B. This enrollment window will end six months to the date after your 65th birthday.

We strongly advise that you apply for benefits during this initial open enrollment period because it is the most advantageous in terms of pricing and because insurers can’t use medical underwriting. In other words, you are guaranteed the absolute lowest prices.

Once the six months have elapsed, you could end up paying much higher premiums or have your covered denied if the medical underwriters decide you’re too risky to cover.

View Plan N Quotes-

View Plan N Quotes-

How Does Medicare Supplement Plan N Compare to Other Medigap Plans?

For starters, Medicare Supplement Plan N offers more coverage compared to Plan L and Plan K. For instance, it covers 100% copayments and coinsurance of Medicare Part B, versus Plans L & K, which only pay 75% and 50%, respectively. The same goes for Medicare Part A deductible.

Furthermore, the only so-called out-of-pocket expenses beyond this monthly premium is the $20 copay that’s needed for office visits and the copay for a trip to the ER for $50, and the Medicare Part B deductible.

Medicare Supplement Plan N vs. Plan G

Right of the bat, it is evident from the comparison table that Plan G offers more protection compared to Plan N. More precisely, Plan G covers two additional areas that Plan N does not.

- Excess Charges: Usually, this is an additional cost charged by some service providers. The majority of healthcare providers accepting Medicare also accept Medicare assignments. The latter is the cost that Medicare states they will pay for that service. However, if the provider wants more money for that service, they will bill you the excess charge, which is only up to an additional 15% of the original cost and Medicare Part B covers the rest.

- Copayments: When you choose Plan N, you are responsible for copays of $20 or more for office visits. It can also be up to $50 if you end up in the emergency room but are not admitted as an inpatient.

Now, in addition to coverage differences between both plans, the cost of both these plans also varies quite a bit. The premiums you can expect to pay for each Plan will vary depending on the carrier you choose, but, Plan G is more expensive than plan N since it offers more coverage.

Even though Plan G has more expensive premiums, it could possibly save you money in the long term. Take, for instance, if you have to make emergency room visits for whatever reason a few times a year, or you end up needing to visit the doctor’s office for treatment, the out-of-pocket expenses, if you have Plan N, can add up quickly and cost you more than if you had Plan G in the beginning.

Medicare Supplement Plan N vs. Plan F

We often get asked what is the best Medicare Supplement Plan in my zip code. However, what many people should be asking is what Medicare supplement is best for their circumstances. Considering your personal circumstances is important, which is why we’ve drafted the following points which should help people choose between Medigap Plan F Vs. Plan N.

Premium prices – The premiums for Plan F and Plan N can vary depending on a couple of factors like age, the use of drugs, tobacco, zip code, and the carrier selling the Plan. So, you need to think if the savings on Plan N is good enough to risk-bearing the extra out-of-pocket expenses?

Your health – Now, if you don’t have to see a doctor daily, it’s possible to save money with Plan N. however, if you soon find yourself having to visit the doctor more often, you’ll end up spending more money compared to if you were to just choose Plan F.

Thinking Ahead – Anyone who wants to change their Plan in the future will be subject to medical underwriting. For those who don’t know, this is a process that insurance companies will use to determine whom they are willing to cover and who they will decline based on their health condition. Most states allow this, which means that the chances are that changing your Plan is going to be near impossible.

Even though the differences between Plan F and Plan N are pretty straightforward, it can still be hard to decide between the two of them. However, it is important to let the math speak for itself. Many online tools will help you compare Plan F and Plan N, helping you make an informed decision when choosing health insurance.

Medicare Supplement Plan N Rate Increase History

Alongside the factors that affect your monthly premium rates, the pricing method that your carrier uses can also impact your premium over time. For example, if your carrier uses a “fixed-rate” pricing method, your premium will increase at a lower rate than if your carrier uses a “variable-rate” pricing method. Over the last 5 years, premiums for Medicare Supplement Plan N increased by 2% to 4% among all insurance companies.

Important Things You Should Know Before Enrolling In Supplement Plan N

Anyone who is new to Medicare and interested in enrolling in Medicare Supplement Plan N or maybe any other Medigap plans should be aware of the 5 things associated with these plans.

- To qualify, you need to be enrolled in both Part A & Part B

- You can choose to have a Medigap Policy or a Medicare Advantage Plan, but you can’t have both. However, you can apply for a Medigap policy if you have the Medicare Advantage plan, but the Medicare Advantage Plan will have to be canceled before the new Medigap policy kicks in.

- A Medigap policy is designed to cover a single individual. If you have a spouse, they will need to have a policy of their own but your spouse can shop among all insurance companies.

- All Medigap policies are guaranteed to be renewed even for those who start having health issues later in life. The insurer can’t cancel the policy if you’re paying the monthly premium.

- The Medigap policies usually include Plan N, but which does not cover everything. Plan N usually excludes dental care, long-term care, hearing aids, skilled nursing facility care if needed, and prescription drugs. You’ll need to join the Medicare Prescription Drug Plan (Part D)

- States that do not permit excess charges from healthcare providers:

Frequently Asked Questions

Which Medigap plan is better G or N?

Medigap Plan G and Plan N are very similar except Plan G covers the Medicare Part B excess charges but Plan N does not so Plan G costs a little more. If you live in one of the states eight states that do not allow doctors to bill you for excess charges, then Plan N will likely be the better choice.

Connecticut

Massachusetts

Minnesota

New York

Ohio

Pennsylvania

Rhode Island

Vermont

What is the deductible for Plan N?

Since Plan N does not cover the deductible for Medicare Part B ($233 for 2022), this amount would need to be satisfied before Plan N pays for Part B charges. This deductible is an annual deductible and typically goes up each year. The Medicare Part B deductible increase for 2022 was the highest annual increase in the last 10 years.

Is Plan N guaranteed issue?

Plan N will not cover Part B deductible. It is often referred to as first-dollar coverage, which has been discontinued for new beneficiaries as of 01 Jan 2020. The only plans covering this deductible are Plan F, C, and High Deductible Plan F.

What is the difference between Medicare Plan G and Plan N?

Medicare Supplement Plan G and Plan N are very similar except for one coverage. Plan G does cover the Medicare Part B excess charges (limit of 15% over the Medicare assigned rates for your healthcare service) but Plan L does not. For this reason, Medigap Plan G costs a little more than Medigap Plan N.

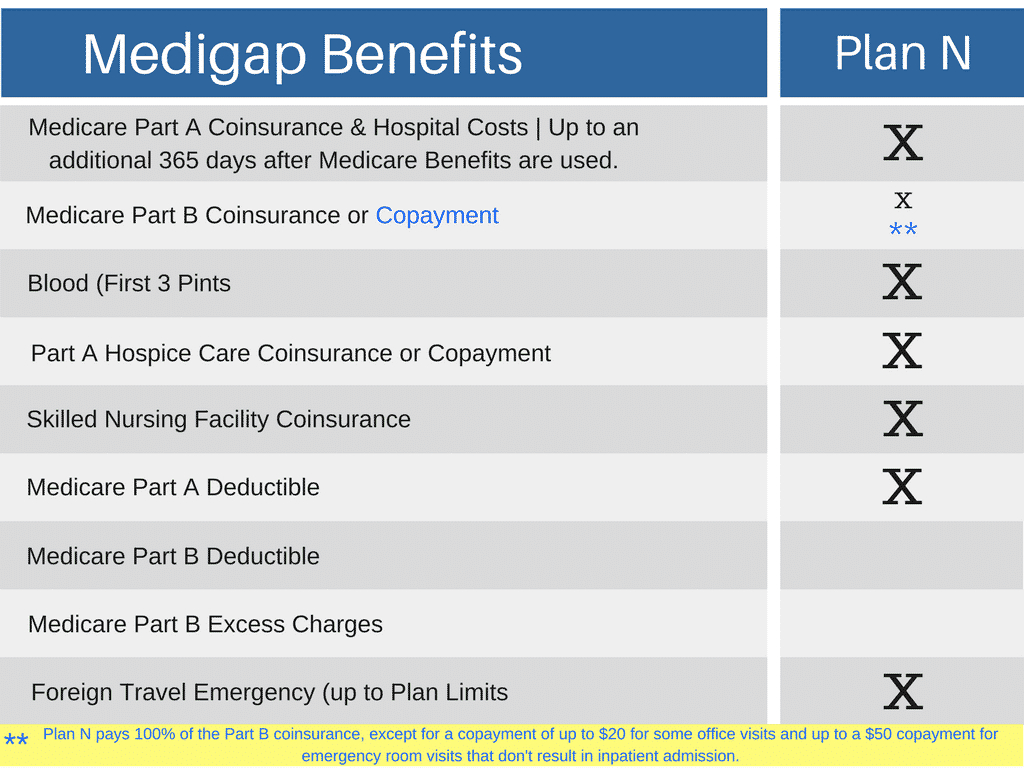

What is Medicare Plan N coverage?

A Medicare Supplement Plan N provides the following coverages:

- Medicare Part A coinsurance and hospital costs: 100%

- Medicare Part B copayment or coinsurance: 100%***

- First 3 pints of blood: 100%

- Medicare Part A hospice coinsurance or copayment: 100%

- Skilled Nursing Facility coinsurance: 100%

- Medicare Part A Deductible: 100%

- Medicare Part B Deductible: no coverage

- Medicare Part B Excess Charges: no coverage

- Foreign Travel Medical Emergencies: 80%

Plan N pays 100% of the Part B coinsurance, except for a copayment of up to $20 for some office visits and up to a $50 copayment for emergency room visits that don’t result in an inpatient admission.

How much does Medigap Plan N cost?

Your Medigap Plan N premiums will depend on various factors like gender, age, geographic location, and health status if you are buying during your open enrollment or a special enrollment period. The average rates across the country for Plan N are between $120 and $180 and are in addition to your Medicare Part B monthly premium.

Is Medicare Plan N better than Plan F?

Your Medigap Plan N premiums will depend on various factors like gender, age, geographic location, and health status if you are buying during your open enrollment or a special enrollment period. The average rates across the country for Plan N are between $120 and $180 and are in addition to your Medicare Part B monthly premium.

Does Plan N AARP cover prescriptions?

Medicare Plan N happens to be one of the most popular plans, and it is offered by some of the largest, most well-known carriers. However, the company you choose ultimately depends on where you live, and the rates being offered.

Does AARP Medicare Supplement Plan N cover dental?

Medicare Supplement plans (Medigap) do not cover retail prescription drugs. If you want prescription drug coverage, you can purchase a Medicare Part D prescription drug plan or a Medicare Advantage plan that includes prescription drug coverage.

What is the difference between Medicare Plan F G and N?

Although Medicare Plan F, G, and N offer similar coverages, there are differences in the benefits they provide:

| Coverage | Plan F | Plan G | Plan N |

| Part A Coinsurance and Hospital Costs | 100% | 100% | 100% |

| Part B Coinsurance or Copayment | 100% | 100% | 100%*** |

| Blood – 1st 3 pints | 100% | 100% | 100% |

| Part A hospice care coinsurance – copayment | 100% | 100% | 100% |

| Skilled Nursing Facility Coinsurance | 100% | 100% | 100% |

| Part A Deductible | 100% | 100% | 100% |

| Part B Deductible | 100%* | X | X |

| Part B Excess Charges | 100% | 100% | X |

| Foreign Travel Emergency Medical | 80% | 80% | 80% |

*** Plan N pays 100% of the Part B coinsurance, except for a copayment of up to $20 for some office visits and up to a $50 copayment for emergency room visits that don’t result in an inpatient admission.

Does Plan N cover Part A deductible?

Plan N does cover the Medicare Part A deductible but will not cover the Medicare Part B deductible.

Does Medigap Plan N cover excess charges?

Medicare Supplement Plan N does not cover the Medicare Part B deductible or excess charges, which are the difference in cost between what a health provider charges for a medical service and the Medicare-approved amount. Medicare Plan N will not cover the copay or coinsurance for doctor’s office and emergency room visits.

The Bottom Line

If you are looking for help navigating the sea of information on Medicare Supplement Plans in order to find the best choice for you, reach out to us at 844-528-8688 or via our online contact form. Our services are always 100% free to you.

Have Questions?

We can Help!

Talk to one of our licensed Medicare supplement agents about the options available to you in your area.

Mon – Fri 8:00 am – 6:00 pm

Sat available upon request