Compare Medicare Supplement Plans

This article gives a brief description of all the available Medicare Supplement Plans, and a Medicare supplement plans comparison chart to help you compare Medigap plans.

Quick and Easy Article Navigation

Click on the plan for a detailed description. To find Medicare Supplement Plan that fits you the best, call for a free no-obligation quote at 844-528-8688. Or continue reading our Medicare supplement comparison.

How to compare Medicare supplement plans

Original Medicare leaves certain “gaps” in your healthcare coverage or out-of-pocket expenses that can be difficult to keep up with on a fixed income. Medicare supplement plans aim to fill these gaps and you will want to compare Medicare supplement plans to find the one that fits you. Here are three of the most common out-of-pocket expenses you can expect to pay if you have Medicare Parts A and B alone:

- Deductibles: This is the amount that you pay for your healthcare services before the healthcare companies do their own part. Deductibles are often the most intimidating number in any health insurance plan.

- Co-payments: These are the costs that healthcare insurance companies don’t pay for, such as charges you pay when you go for a doctor’s visit. They are not usually very expensive but can add up over time.

- Coinsurance: This is the amount that you are required to pay in conjunction with the insurance company to cover the cost of your healthcare bills. This may sound like a copayment but it is different because coinsurance is usually a percentage of the service charge, while co-payments are a flat fee.

What Will Medicare Supplement Plans Cover?

Original Medicare has a lot of “gaps” that you are left to pay out of your own pocket. If you don’t like the idea of surprise charges, there are many reasons you should consider Medicare Supplement Plans for the peace of mind they can provide. When you look at the Medicare supplement plans comparison chart, you will see different plans cover different costs, so it is very important to compare Medigap plans for the benefits you need and want.

Here are just a few of the benefits that Medicare Supplement Plans can offer.

- Part A Hospital Deductible. The most popular Medigap plans cover the deductible for hospital stays and other care that falls under Part A. For 2018, that protects your wallet from $1,556.00 in unexpected costs every benefit period.

- Part B Coinsurance / Co-payment. Under Original Medicare, you will be responsible for 20% of the cost of most non-preventative medical services. This means that if you needed a procedure billed at $2,000, you would have to pay $400 and Medicare would cover the rest. Most Medigap plans, however, cover this coinsurance completely so that your out-of-pocket expenses would be zero.

- Foreign Travel Emergency. You might not realize that your Medicare benefits don’t extend beyond the boundaries of the United States. With the right Medicare Supplement Plan, you can still get coverage for emergency services that happen while you’re traveling the world. You just need to meet a $250 deductible and Medicare will cover 80% of the charges after that.

- Blood. Original Medicare does not cover blood transfusions that you may need. All of the Medigap plans, on the other hand, cover the first three pints of blood that you need annually (Plans K and L only cover 50% and 75%, respectively).

- Extended Hospital Stay. Original Medicare will only cover 60 days in a hospital, after that the expense to you can add up quickly ($335 daily for days 61 – 90, and $670 daily after that). All Medigap plans cover up to 150 days of each benefit period, plus an additional 365 days in your lifetime.

EASILY COMPARE PLANS AND RATES

EASILY COMPARE PLANS AND RATES

Medicare Supplement Plan Comparison Chart

Medicare Supplement Plans plans don’t cover everything. Specifically, they don’t pay for charges such as long-term medical care, dental treatment, hearing aids, prescription glasses, or prescription drugs.

When looking at the Medicare supplement plans comparison chart, there are currently 10 standard Medicare Supplement Plans as you can see from the Medicare supplement plans chart below. They are labeled A through N (E, H, I, and J are no longer available to new subscribers). The costs of plans may differ with each insurance company, but the benefits are same across the board. The Medicare supplement plan comparison chart below shows, a list of plans and the benefits offered. Keep reading to compare Medigap plans and see what plan fits your needs and budget.

The Medicare supplement plans comparison chart below shows basic information about the different benefits Medigap policies cover.

Yes = the plan covers 100% of this benefit

No = the policy doesn’t cover that benefit

% = the plan covers that percentage of this benefit

N/A = not applicable

* Plan F also offers a high-deductible plan. If you choose this option, this means you must pay for Medicare-covered costs up to the deductible amount of $2,300 before your Medigap plan pays anything.

** After you meet your out-of-pocket yearly limit and your yearly Part B deductible, the Medigap plan pays 100% of covered services for the rest of the calendar year.

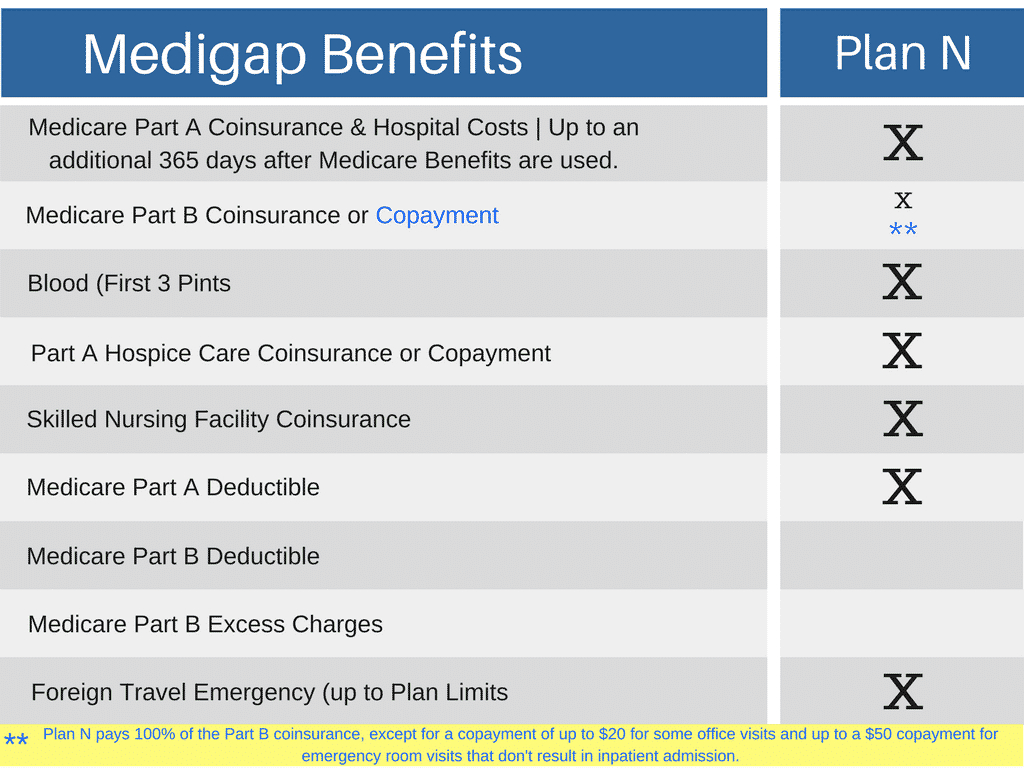

*** Plan N pays 100% of the Part B coinsurance, except for a copayment of up to $20 for some office visits and up to a $50 copayment for emergency room visits that don’t result in inpatient admission.

Starting January 1, 2020, Medigap plans sold to new people with Medicare won’t be allowed to cover the Part B deductible. Because of this, Plans C and F will no longer be available to people new to Medicare starting on January 1, 2020. If you already have either of these 2 plans (or the high deductible version of Plan F) or are covered by one of these plans before January 1, 2020, you’ll be able to keep your plan. If you were eligible for Medicare before January 1, 2020, but not yet enrolled, you may be able to buy one of these plans.

You live in Massachusetts, Minnesota, or Wisconsin

If you live in one of these 3 states, Medigap policies are standardized in a different way.

Medicare Supplement Comparison

Below is a brief description of all the Medicare supplement plans offered today. To fully Compare Medicare Supplement Plans, just click on the blue type for a detailed explanation. Medicare Supplement Plan G and Plan N are the two most popular.

Medicare Supplement Comparison – Plan A

This is the most basic of the Medicare supplement plans, and Medicare Supplement Plan A is required to be offered by any providers who wish to offer Medigap. Plan A is an affordable option but covers far less than the others.

Plan A is typically recommended for Medicare enrollees who are very healthy and do not expect to see health care providers as frequently as other seniors and for those enrollees who are on a very tight budget. Although the Medicare Part A and Part B deductibles may not be an extreme financial setback for many seniors, the Part B coinsurance of twenty percent can add up quickly and result in significant out-of-pocket expenses. Medicare Supplement Plan A takes care of the Medicare Part B coinsurance and co-payment, the first 3 pints of blood that Medicare does not cover, and takes care of the coinsurance costs for Hospice Care that is not covered under Medicare Part A.

Medicare Supplement Comparison – Plan B

Medigap Plan B covers all of the same coverage gaps as Plan A plus the Original Medicare Part A deductible. This plan is an ideal choice over Plan A because it will protect you from high charges due to emergency situations and it is still one of the most affordable plans available.

Since the Medicare Part A deductible is the difference between Plan A and Plan B, it’s important that seniors understand how much it is and how it works. Most consumers assume a deductible applies annually and unfortunately with Medicare Part A, such is not the case. The Medicare Part A deductible for 2022 will be $1556.00 per benefit period, not per year.

A benefit period is defined as a period that begins the day you enter a hospital or skilled nursing period and it ends when the patient has not received any inpatient hospital care or skilled nursing facility care for 60 consecutive days. This means there isn’t a limit on how long a benefit period might last and there is no limit on the number of benefit periods. This means that the $1556.00 deductible can be charged multiple times per year. And by the way, there is also coinsurance charged under Medicare Part A if your benefit period goes on for 61 or more days.

Medicare Supplement Plan C

Medicare Supplement Plan C covers almost all possible out-of-pocket expenses, making it one of the most all-inclusive Medigap plans available. The only option that goes further than Plan C is Medigap Plan F.

The one coverage gap that Plan C does not cover is the possible excess charge for your medical provider. Excess charges result from having a primary doctor or specialist who charges more than the Medicare Part B assigned fee. Read more about part B excess charges here.

This means the patient is responsible for the difference between what your physician (only if they are not assigned by Medicare) charges and what Medicare Part B will pay but with a maximum of 15%. Some states do not allow excess charges by physicians because of a law called the Medicare Overcharge Measure. The states that have adopted the Medicare Overcharge Measure are:

- Connecticut

- Massachusetts

- Minnesota

- New York

- Ohio

- Pennsylvania

- Rhode Island

- Vermont

Knowing this, residents of the above mentioned states would be better off financially purchasing Plan C over Plan F since the excess charge coverage is the only difference and since Plan C has a lower premium.

Medicare Supplement Plan D

Medicare Supplement Plan D covers most of the cost that is not covered in plan A and B. It is slightly less comprehensive than Plan C because it still leaves you responsible for the Part B Deductible (which is relatively low) and Part B Excess Charges (which are rare) and in some states illegal. The Medicare Part B deductible of $233.00 is much lower than the Medicare Part A deductible and most policyholders do not pay the additional monthly premium to cover it.

Note:

Medicare Supplement Plan F, will not be offered to people entering Medicare in 2020.

Medicare Supplement Plan F

Medicare supplement plan F is both the most expensive but also the most comprehensive Medigap option available when you compare Medicare supplement plans. At the cost of high monthly premiums, recipients are left with practically no surprise out-of-pocket charges. Plan F also has a special high deductible version that comes with a more affordable premium as long as you are willing to cover an annual deductible first.

Medicare Supplement Plan F is for enrollees who prefer not to have any out-of-pocket health care expenses except for the Medicare Part B monthly premium and the Medicare Supplement Plan F monthly premium.

Medicare Supplement Plan F (High Deductible)

Plan F also has a special high-deductible version that comes with a more affordable premium as long as you are willing to cover an annual deductible first. This is the lowest cost of all the Medicare Supplement Plans. This deductible changes every year, if you choose this option, this means you must pay for Medicare-covered costs (coinsurance, copayments, and deductibles) up to the deductible amount of $2,240 in 2018 before your policy pays anything. See our full article HERE

Medicare Supplement Plan G

The Medicare Supplement Plan G covers the full cost of out-of-pocket expenses such as coinsurance, excess charges, and copayments. The only thing not covered is the Medicare Part B deductible. At this time Plan G offers the most benefits for the lowest premium of the Medicare Supplement Plans. Remember to take a hard look at plan G when you compare Medicare supplement plans.

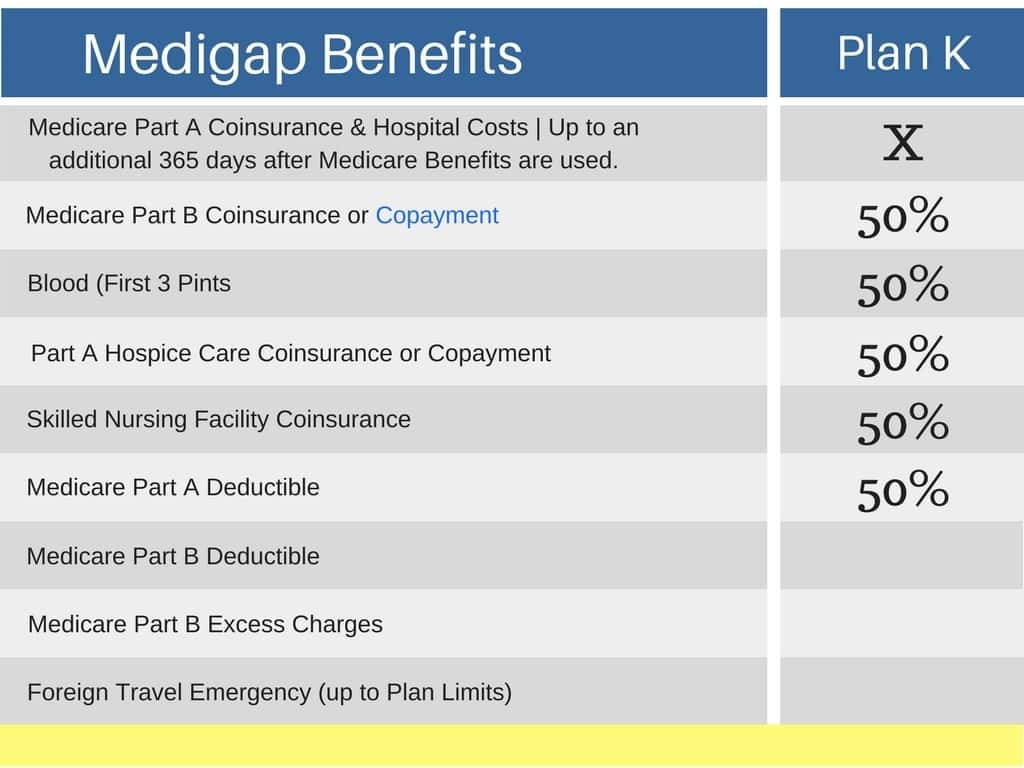

Medicare Supplement Plan K

If you want a low-cost Medigap plan with basic coverage, then this is the plan for you. The Medicare Supplement Plan K will pay up to 50% of your fees for most covered services until you reach the plan limit, after which you no longer have to pay anything.

Medicare Supplement Plan L

Medicare supplement plan L is basically the same as Plan K except it covers 75% of the charges and has a lower out-of-pocket limit.

Medicare Supplement Plan M

Medicare Supplement Plan M is mostly identical to Plan D. The only difference is that Plan M only covers 50% of the Part A deductible, leaving you at a slightly increased risk of high emergency charges

Medicare Supplement Plan N

Medicare supplement plan N is another Plan D lookalike. Plan N, however, includes co-payments of $20 for office visits and $50 for ER services. This Plan also does not cover the Medicare Part B Excess charges.

Considerations When Doing A Medigap Plans Comparison

- You must have Original Medicare (parts A and B) in order to enroll in Medicare supplement insurance.

- You cannot have Medigap and a Medicare Advantage Plan (Part C) at the same time. You can apply for a Medigap policy while on a Medicare Advantage plan but must make sure to exit the Advantage Plan before starting on Medigap.

- Medigap comes with its own monthly premium, and you must still pay your Part B premium. Compare Medicare supplement plans to see what fits your budget.

- Each Medigap policy covers an individual. Spouses, therefore, must purchase their Medicare supplements separately.

- Medigap is provided by private insurance companies that are licensed to sell Medicare supplemental insurance plans. They don’t all offer every single plan, but the benefits of the plans they do offer will be identical.

- There are 3 types of rating types of Medicare supplement plans, attained age, issue age, and community-rated plans. You can read our full article on these by clicking here.

- All Medicare supplements will have rate increases. Read the full article on Medigap rate increases by clicking here.

- Your Medicare supplement doesn’t cover prescription drugs. You’ll need to obtain Medicare Part D for prescription coverage.

- Insurance companies can’t end your coverage due to health conditions once you are enrolled.

Who Can Get a Medicare Supplement Plan?

If you are thinking of getting a Medicare supplement, then you should be aware that you can‘t get it without the Original Medicare plan. This is because as the name suggests these are supplement plans. They are supplementing the benefits of Parts A and B.

Anyone with Original Medicare, therefore, is eligible for Medigap. In order to qualify for Original Medicare, you must meet one of the following criteria:

- Age 65+

- Diagnosed with permanent kidney failure (End-Stage Renal Disease), necessitating dialysis or transplant

- Have received disability from Social Security or Railroad Retirement Board for 24 concurrent months

- Diagnosed with ALS (Lou Gehrig’s disease)

Enrolling In Medicare

If you are receiving Social Security: You will be enrolled in Medicare Parts A and B automatically when you turn 65, and your Medicare Card will be sent to you approximately 90 days before your birthday.

If you are NOT receiving Social Security: You will need to enroll in Medicare by contacting the Social Security Office.

Medicare Supplement Open Enrollment

The Medicare supplement open enrollment period lasts for six months, beginning on the first of the month that you are 65 or older (once you are enrolled in Medicare Part B).

It’s very important to enroll during this period in order to avoid cumbersome underwriting and potentially higher premiums or denial of coverage due to health conditions, of course, it is never too early to compare Medicare supplement plans, so you have a plan going in.

View Mediagap Quotes-Enter Your Zip Code:

View Mediagap Quotes-Enter Your Zip Code:

Can I Get Medigap Before I Turn 65?

While insurance companies are not federally mandated to offer Medicare supplements to Medicare recipients who are under 65, many states do mandate this to some extent, and most insurance companies offer some sort of Medicare supplement for people in this situation. However, because the federal guidelines are not as strict for under 65 Medicare recipients, insurance companies may charge you higher premiums and require health screening and medical underwriting.

Difference Between Medicare Supplement Plans and Medicare Advantage Plans

Navigating Medicare can be difficult. There are Parts A, B, C, and D but also Plans A, B, C, and D. Sometimes you’ve got a deductible, and sometimes you don’t. Sometimes you pay coinsurance, sometimes it’s a co-payment.

Perhaps one of the biggest confusions for new Medicare recipients is figuring out the difference between Medicare Supplement Plans and Medicare Advantage Plans.

While Original Medicare is distributed through the federal government, Medicare Supplement Plans and Medicare Advantage Plans are both sold by private insurance companies. They sound similar but are different in the kind of coverage they provide.

Medicare Supplement Plans work with your original plan (Parts A and B). If you have Medigap, then you also have Original Medicare. Your supplement just fills in some of the “gaps” left by Parts A and B. Medicare Advantage Plans (Part C), on the other hand, are a replacement for Original Medicare. Instead of sticking with Parts A and B, you choose to get all of your coverage from a private insurer. Since you don’t have Original Medicare, you can’t receive Medigap while you are enrolled in a Medicare Advantage Plan.

Have Questions?

We can Help!

Talk to one of our licensed Medicare supplement agents about the options available to you in your area.

Mon – Fri 8:00 am – 6:00 pm

Sat available upon request

Enroll in Your Medicare Supplement Plan Before It’s Too Late

Remember that you could be denied coverage or pay higher premiums if you miss open enrollment. If you are considering a Medigap plan but don’t know which of the Medicare Supplement Plans to pick, or if you’re just intimidated by the whole process, we’re here to help compare Medicare supplement plans and through the enrollment process.

Frequently Asked Questions

Medigap, also known as Medicare Supplement Insurance, is a type of private health insurance policy that is designed to fill in the “gaps” left by Original Medicare (Part A and Part B) coverage. These gaps can include out-of-pocket costs like deductibles, copayments, and coinsurance. Medigap policies are sold by private insurance companies, and they are standardized by the federal government, meaning that each plan type (e.g., Plan A, Plan B, etc.) provides the same coverage, regardless of the insurer.

Plan G, on the other hand, is one specific type of Medigap plan. It is often considered one of the most comprehensive Medigap plans, as it covers all of the gaps in Original Medicare except for the Part B deductible. This means that with a Plan G policy, you would generally not have to pay any out-of-pocket costs for Medicare-covered services beyond your monthly premium.

In summary, Medigap refers to a broad category of private insurance policies that can help fill in the gaps in Original Medicare coverage, while Plan G is one specific type of Medigap policy that provides comprehensive coverage but does not cover the Part B deductible.

When comparing Medicare Supplement insurance plans, there are a few key factors to consider. First, you’ll want to look at the coverage offered by each plan type to determine which one best meets your needs. It’s also important to consider the cost of each plan, including the monthly premium and any out-of-pocket costs like deductibles or copayments. You may also want to consider factors like the insurer’s reputation and customer service track record.

To compare plans, it can be helpful to use an online comparison tool or speak with a licensed insurance agent who can provide personalized guidance based on your specific needs and budget. When evaluating different plans, it’s important to take the time to carefully review the details of each policy and ask any questions you may have to ensure that you are making an informed decision about your healthcare coverage.

Medicare Supplement plans, also known as Medigap plans, are designed to help cover the out-of-pocket costs that Original Medicare (Part A and Part B) doesn’t cover. There are 10 standardized Medigap plans available in most states, labeled A through N, each providing a different set of benefits. The most comprehensive Medigap plan is Plan F, which covers all of the out-of-pocket costs that Original Medicare doesn’t cover, including deductibles, copayments, and coinsurance. However, Plan F is only available to people who became eligible for Medicare before January 1, 2020. For those who became eligible for Medicare after that date, the most comprehensive Medigap plan is Plan G, which covers everything that Plan F does except for the Medicare Part B deductible.

For 2022, Plan K and Plan L are the only plans that have a limit on out-of-pocket expenses. The limit for Plan K is $6,620 and the limit for Plan L is $3,310.

There is no difference between a Medicare Supplement and a Medigap plan. “Medicare Supplement” is another term for Medigap, and both terms refer to private health insurance policies that are designed to fill in the gaps left by Original Medicare (Part A and Part B) coverage. These gaps can include out-of-pocket costs like deductibles, copayments, and coinsurance.

Medigap policies are sold by private insurance companies, and they are standardized by the federal government, meaning that each plan type (e.g., Plan A, Plan B, etc.) provides the same coverage, regardless of the insurer. The terms “Medicare Supplement” and “Medigap” can be used interchangeably to refer to these types of policies.

Give us a call at 844-528-8688 or fill out our easy contact form and we’ll help you compare Medicare supplement plans, and there is never a fee for our services.

Have Questions?

We can Help!

Talk to one of our licensed Medicare supplement agents about the options available to you in your area.

Mon – Fri 8:00 am – 6:00 pm

Sat available upon request