Today, Medicare is made up of four distinct parts. In order to make the best choices, it’s helpful to understand each part and how it will benefit you. Here, we’ll discuss the four parts of Medicare.

Easy Article Navigation

Traditional Medicare consists of part A, Part B, Part C, and Part D. If you understand each of these parts of Medicare, you are on your way to choosing the healthcare insurance that is right for you.

Medicare Part A

If you’re healthy, you might not think about why you need Part A coverage. But if you ever need hospital treatment in the future and don’t have proper coverage, the cost can quickly add up. Under Part A, your hospital stays are covered, as well as other important services and amenities like hospital meals, some types of rooms, lab tests, x-rays, and more.

Part A alone won’t cover everything. That’s why it’s important to enroll in both Parts A and B.

Medicare Part B

Let’s talk about the benefits of Part B. This Medicare plan provides you with access to specialist services and preventive healthcare. As we age, we are more at risk of acquiring chronic diseases.

Some things that might be covered by Part B include your annual physical exam, laboratory tests when you visit the doctor, mental healthcare, and other hospital-related expenses.

What if I put off Enrolling in Part B?

If you delay enrolling in Part B, you will generally have to pay a monthly late enrollment penalty. It’s important not to wait because the Part B late enrollment penalty lasts for life.

Medicare Part C

Part C is Medicare Advantage, which is private insurance. A Medicare Advantage plan includes all of the benefits of Parts A and B but entails a monthly premium. Medicare Advantage often includes prescription drug coverage, dental, vision, and hearing benefits. It may come with other perks as well such as gym memberships.

Part C is just one of many options for Medicare coverage. Many beneficiaries find Medicare Advantage plans attractive because their relatively low premiums and all-inclusive nature are a good option for additional coverage. After studying your options carefully, you might decide that Part C or Medigap is best for you.

Rather than supplementing your Medicare coverage like Medigap will do, Part C (Medicare Advantage) your part A and B will be administered by the insurance company and most times your part D will be included.

Medicare Part D

If you haven’t taken any prescription medications recently, you might not know why you would need prescription drug coverage. However, the benefits of this plan extend into the future, when you might need prescriptions. When you do, you will be covered and have a lower out-of-pocket cost.

If you enroll in a Part D prescription drug plan, you’ll pay a monthly premium. In exchange, your out-of-pocket costs for prescriptions will be lower.

When you sign up for a Part D prescription drug plan, you’ll pay a monthly premium. For every month that you stay enrolled, your co-pays will be lowered.

What If I put off signing Up for Medicare Part D?

Part D also charges late enrollment penalties when you miss the deadline for signing up. These penalties are added to your monthly premium, even if you don’t take any prescription medications. This penalty stays with you as long as you are on the plan.

What about the out-of-pocket Expenses that Result from Medicare?

Although Original Medicare provides comprehensive healthcare coverage for seniors 65 or older, there are considerable gaps in coverage that can result in considerable out-of-pocket expenses.

To fill these out-of-pocket expense gaps, private insurance companies offer Medicare Supplement Plans (Medigap) that help Medicare enrollees to mitigate their out-of-pocket expenses.

Currently, there are 47 states that allow the 10 standardized Medicare Supplement plans to be sold within their borders. Adding just one of these 10 Medicare supplements (Medigap) plans can reduce your out-of-pocket healthcare expenses considerably.

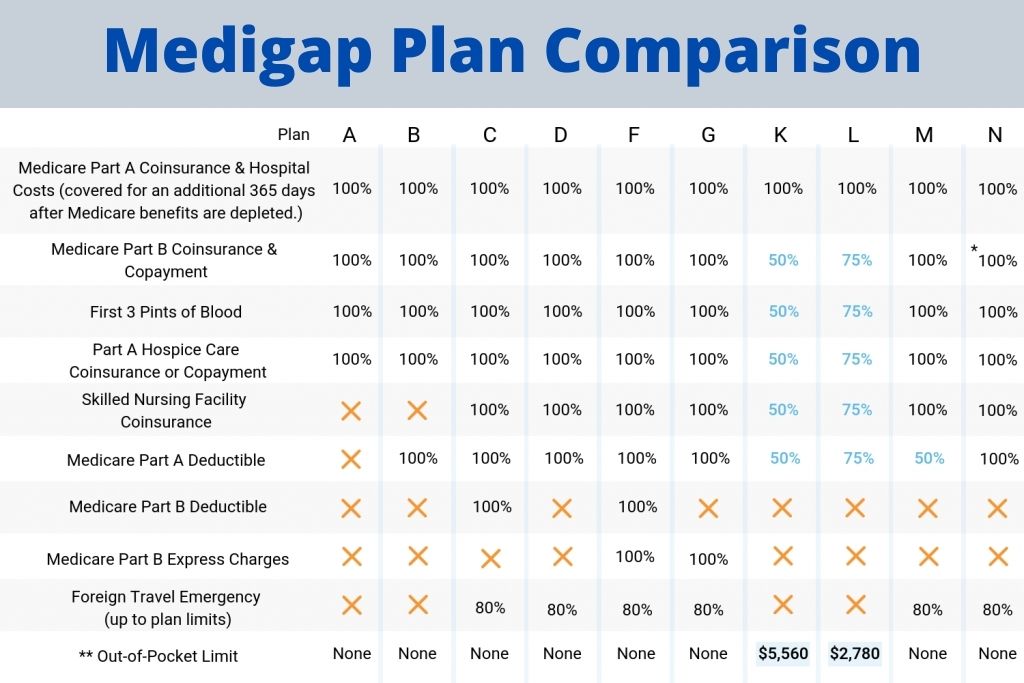

The 10 Standardized Medicare Supplement Plans for 2022

Most seniors will need every part of Original Medicare to mitigate their healthcare costs. Each Medicare Supplement Plan (A to N) can help seniors enrolled in Original Medicare to reduce their out-of-pocket healthcare expenses.

In fact, Plan K and Plan L contain an out-of-pocket limit. When the limit is reached during a calendar year, Plan K or Plan L will begin covering your healthcare costs at 100%.

Considering a Medicare Plan?

Get online quotes for affordable Medigap insurance

How to know which Medigap Plan is Right for Me?

Original Medicare and Medicare Supplement insurance can be confusing. Finding a Medigap plan that is right for you should be based on your current health situation and your budget.

Keep in mind, however, most seniors develop certain health issues that may be costly to manage and under these conditions, Medicare Supplement Plan G and Plan N will likely mitigate your out-of-pocket expenses and provide peace of mind knowing that you can get the healthcare needed when a severe or chronic health issue presents itself.

What about Medicare Advantage?

Like Medicare Supplement insurance, a Medicare Advantage Plan (Medicare Part C) can help reduce the out-of-pocket expenses that you’ll need to contend with because of the coverage gaps in Original Medicare Part A, Part B, and Part D.

Unlike Medigap which supplements your Original Medicare, Medicare Advantage replaces your Original Medicare and is administered and sold by private insurance companies.

Not only will Medicare Advantage fill the gaps in Original Medicare, but the plan will also typically provide coverage for prescription drugs, dental, hearing, and vision expenses.

Moreover, most companies offer additional benefits like over-the-counter vitamin benefits, a gym membership, and medical transportation.

Which is Better for Me? Original Medicare, Medigap, or Medicare Advantage?

Shopping for health coverage when you’re a senior can be confusing and even a little aggravating. However, if you’ll take a few minutes out of your day and discuss your circumstances and budget with an independent Medicare specialist, you’ll have a better chance of determining which plan is best for you and will mitigate ever-increasing out-of-pocket expenses.

Frequently Asked Questions

Part D charges late enrollment penalties when you miss the deadline for signing up. These penalties are added to your monthly premium, even if you don’t take any prescription medications. This penalty stays with you as long as you are on the plan.

Medigap Plans K and L have an out-of-pocket limit that can help you keep your healthcare expenses under control. Once you’ve reached your limit, the Medigap plan will then pay 100% for the remainder of the year.

Medicare Part A covers hospital expenses, skilled nursing facilities, hospice, and some home health care services. Medicare Part B covers outpatient medical care such as doctor visits, x-rays, bloodwork, and routine preventative care. Both are subject to deductibles and coinsurance.

Yes. Most people do not pay a monthly premium for Medicare Part A (hospital coverage) if they have worked and paid Medicare taxes for 40 quarters before turning age 65.

Have Questions?

We can Help!

Talk to one of our licensed Medicare supplement agents about the options available to you in your area.

Mon – Fri 8:00 am – 6:00 pm

Sat available upon request